Overview

China is now the largest official creditor to low- and middle-income countries. As grace periods expire and global interest rates remain elevated, many sovereign borrowers face peak repayment obligations to Chinese state-owned lenders.

Yet most publicly available data still capture what was promised at signing—not what has actually been disbursed, repaid, deferred, capitalized, or restructured over the life of a loan. Even systems specifically designed to monitor sovereign borrowing, such as the World Bank’s Debtor Reporting System (DRS), face significant structural limitations. Recent research demonstrates that roughly half of China’s official lending commitments to public and publicly-guaranteed (PPG) borrowers are either unreported or not attributed as sources of external debt to Chinese creditors in the DRS. Moreover, the DRS provides information only at an aggregate level, preventing loan-level verification and forcing analysts to rely on opaque, “black-box” reporting rather than independently traceable cash-flow data.

Without accurate, loan-level performance data:

- Sovereign exposure is mismeasured.

- Debt sustainability analyses rely on unrealistic assumptions.

- Liquidity risks are underestimated.

- The solvency implications of restructurings remain opaque.

Understanding the financial performance of China’s cross-border loans is now central to sovereign risk assessment and early detection of financial distress and default in the Global South.

Licensing and Updates

The next iteration of the dataset (3.0) will be available for licensing in the fall of 2026, and will cover loan commitments through December 31, 2023 and debt restructuring through mid-2026. The Chinese PPG Loan Performance Dataset 2.0 is a proprietary research product developed by AidData. It is not currently scheduled for public release.

Institutional access is available through tailored licensing arrangements designed to support policy analysis, risk assessment, and program design. Please contact Brooke Escobar at bescobar@aiddata.org for more details.

Dataset Scope and Architecture

A uniquely detailed and comprehensive source of evidence

AidData’s Chinese PPG Loan Performance Dataset 2.0 addresses this major evidentiary gap. It is a loan-level dataset that tracks the disbursement, repayment, arrears, restructuring, and outstanding debt trajectories of PPG loans issued by Chinese state-owned creditors to low- and middle-income countries. For all loans formally issued between 2000 and 2022, it captures financial performance information (disbursements, repayments, restructuring events) between January 2000 and March 2025.

The dataset provides dynamic amortization schedules that reflect each loan’s full life cycle, including three parallel amortization schedules:

- T0 Planned Schedule, reflecting the repayment path implied by contractual terms at signing.

- Perfect Compliance Schedule, incorporating actual disbursement details and prevailing benchmark interest rates under the assumption of full and timely repayment.

- Actual Performance Schedule, integrating observed disbursements, repayments, arrears, restructurings, and time-stamped outstanding balances to measure actual performance over time.

For institutions that monitor public debt exposure, evaluate sovereign credit risk, or design debt relief operations, the dataset offers a uniquely detailed and comprehensive source of evidence.

Each loan's three amortization schedules roll up into a standardized set of loan-level summary statistics, reported in both nominal USD and net present value terms (discounted at 5% from the year of commitment). Reporting every metric under all three models gives users a direct view of how borrowing costs and concessional depth shifted from what was promised at signing to what the borrower actually experienced.

The summary statistics cover the headline financial flows for each loan: total disbursements, total principal repayments, total interest paid, and total fees (commitment, management, and insurance). For loans that have encountered repayment difficulties, the Actual Performance summary also captures cumulative principal and interest arrears, interest recapitalized into principal during restructuring events, and any debt forgiveness granted by the creditor. Together, these fields make it possible to quantify, loan by loan, the gap between expected and realized debt service.

Three derived metrics translate the underlying flows into standardized indicators of loan cost and concessionality. The all-in cost of borrowing expresses the sum of interest, fees, and recapitalized interest as a share of total disbursements—a single figure that captures the full economic price of credit, including costs that emerge only after arrears or restructuring events. The OECD grant element and grant equivalent measure the concessionality of each loan against internationally recognized benchmarks. Calculating all three indicators across the three models allows users to observe how restructurings, arrears, and rate movements alter a loan's true cost and concessional value over its lifetime.

The evidentiary base behind these metrics is substantial. In total the dataset covers 3,719 PPG loans across 124 low- and middle-income countries, supported by over 15,000 direct loan performance observations drawn from official government and creditor sources.

The dataset covers 3,719 PPG loans across 124 low- and middle-income countries, supported by over 15,000 direct loan performance observations drawn from official government and creditor sources.

.png)

The summary statistics cover the headline financial flows for each loan: total disbursements, total principal repayments, total interest paid, and total fees (commitment, management, and insurance).

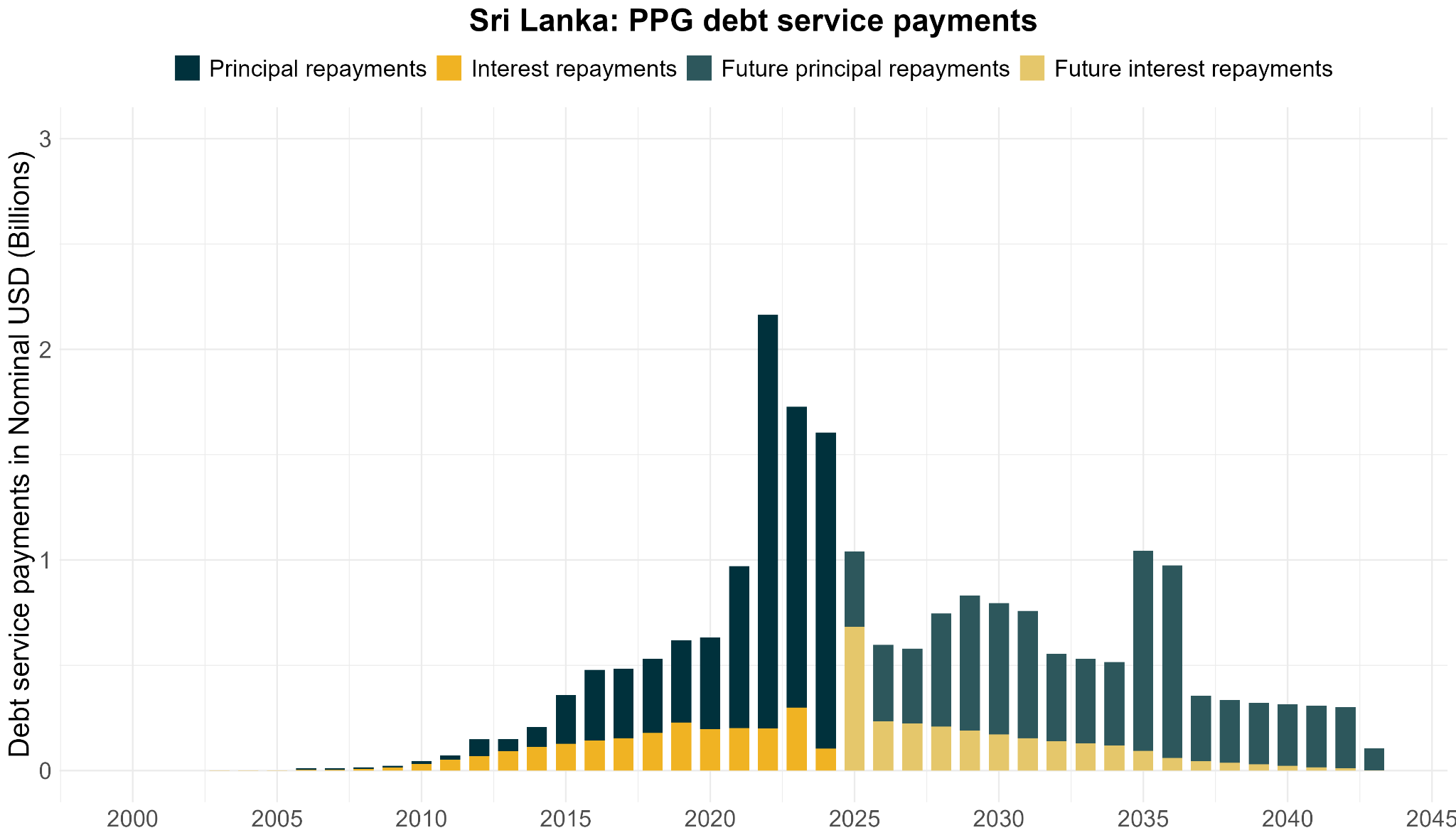

Case Study

Kenya’s USD-to-RMB Debt Conversion Was Really a Restructuring

When Kenya announced in October 2025 that it had converted its Standard Gauge Railway debts to China Eximbank from U.S. dollars (USD) into Chinese renminbi (RMB), the move was widely framed as a breakthrough for RMB internationalization and a clever way to reduce borrowing costs. Early reporting suggested the switch could save Kenya roughly $215 million a year due to interest rate reductions associated with RMB.

But this narrative does not tell the full story.

In a new policy note, AidData researchers Sailor Miao and Oshin Pandey and find that the largest source of debt relief did not come from the benchmark rate change alone.

Reflecting over decade of independent thought leadership on China, economic statecraft, and sovereign debt

Research Team

For technical or research inquires, contact:

Bradley C. Parks

Executive Director

Brooke Escobar

Associate Director of Tracking Underreported Financial Flows (TUFF)